Thread:

Thread:

A Review on electronic money

Definition of electronic money:

Define it as: Cash value stored on a prepaid electronic device that is not linked to a bank account, and used as a payment tool.

The IMF defines it as: monetary value in the form of credit units stored in electronic form or in electronic memory for the benefit of the consumer.

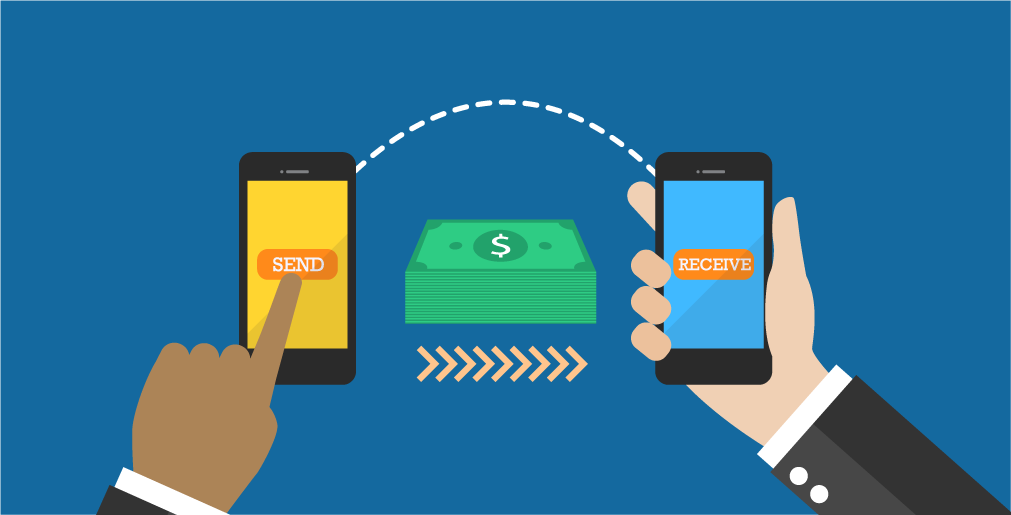

It is therefore money stored by algorithms in processors, and other computers can carry out online loyalties as an alternative to coins and paper currencies that they of course cannot send over the Internet.

Also known as a set of digital protocols and signatures that allow the e-mail to actually replace the exchange of traditional currencies.

Electronic or digital money is the electronic equivalent of traditional money that we used to trade.

When holding cash on an electronic holder that can be used according to two systems:

A- On-line system:

This system means that the consumer does not personally have electronic cash, but entrusts payments to a third party, which is the bank in charge of this task, where the bank handles all transfers of electronic cash, and holds the consumer's cash accounts as this system also works to ask the merchant to contact the consumer bank to receive payment for consumer purchases, which helps to prevent fraud by confirming the monetary authority of the consumer.

B- Off-line system:

In this system the customer's card is read through a computer positioned with the merchant, and the amount of purchases is deducted through this card as it contains either a memory that stores information on the client's account or on magnetic runways where the maximum amount that cannot be exceeded within a week, for example, is specified by the bank.

The nature of electronic money:

Economists' views are clearly different in determining the nature of e-money and we will try to highlight these divergent views.

First opinion: Electronic money is an immaterial dye for paper money

There is no doubt that money is a symbol that represents value and not value itself and today electronic money is the most modern and complex picture of money and perhaps the fundamental difference between it and the types of money before it is that it no longer takes a physical form but is the transfer of information between the parties of exchange, information about money has become more important than the money itself.

On this basis, electronic money is an immaterial form of paper money, as its issuance is to convert the form of money from the paper version to the electronic version, so that the issuing institution will have equality between (input money) as traditional money to be solved until the card is shipped and (output money) as electronic money with which the card is shipped.

Second opinion: Electronic money is an exchange tool, not a payment tool

This view considers the issuance of electronic money as a kind of sale of the source's assets because it is purchased from the source for an equivalent amount of conventional money or in other words the electronic money issues are purchased with the equivalent of central bank money, because there is money purchased by other money, and at the end of the e-money life cycle the source who recovers it acts as a buyer from the sellers who received it for their sales and according to the above, the issuing institutions are obliged to keep the (traditional) money received in return for the last electronic money ( the latter) electronic money. Just take the other money.

Third opinion: Electronic money is a credit tool

The owners of this opinion consider that all types of money are forms of credit, which are also used as a means of exchange, which facilitates the conduct of various transactions either electronic money as a cash balance registered electronically on a value-added card, it is also considered credit because this balance is a kind of debt to its source and the legal obligation of the card issuer towards the holder of the electronic cash and digital units registered on the card is similar to the fact, the government's legal obligation in the face of the currency is the currency itself.

Fourth opinion: Electronic money virtual images of tripolar flow

According to this view, the life of electronic money goes through three stages:

1. Issue for cardholder.

2. Move from the card holder to a third party such as the seller to whom the e-money has been transferred.

3. The destruction of electronic money by third party recovering from traditional money from the source and it should be remembered that the issuance of electronic money is not considered a normal account of a financial nature, the fact that the issuance process and the destruction of electronic money are recorded outside the budget in the information base and therefore the electronic money dealers consider the information recorded in this account to be more of an information altruistic than financial.

E-money characteristics:

E-cash for other electronic payment tools is characterized by the following characteristics:

A. Usage characteristics:

• Retains value as independent digital information from any bank account.

• Allows value to be transferred to someone else by financing digital information.

• Allows remote transfer over the Internet or wireless network.

• Does not require a third party to show or review and confirm the exchange.

• Split and available in the smallest possible cash units to facilitate low-value transactions.

• Fits with low-value transactions because exchange expenses are usually minimal.

• It is characterized by the fact that it is available to all times and circumstances to suit the global nature of the Internet.

• Designed to be easy to use compared to other payment methods, ease of use is an attractive factor in consumers' acceptance of any e-money system.

B. Safety and reserve characteristics

• Secure when used so that it is difficult to hack through by hackers.

• Its dealers are able to verify its validity and it has not been acted upon by others.

• Allows each of the parties to verify the truth of the other party, which is usually the case when using the electronic signature and the keys to the public and private code.

• Characterized by the ability to work continuously and operate in all circumstances in order to preserve the rights of its customers.

• Confidence in dealing is achieved in such a way that customers are unable to deny that they make money after it has been completed.

Thanks

Thanks Currently Active Users

Currently Active Users Forex Forum India Statistics

Forex Forum India Statistics